Life insurance helps make sure your loved ones are protected if something happens to you, so they can move forward without added financial stress. Here’s a look at the basics and how life insurance could work for your family.

Life insurance generally pays a tax-free payout, called a death benefit, to your chosen beneficiaries if you pass away while the policy is active.

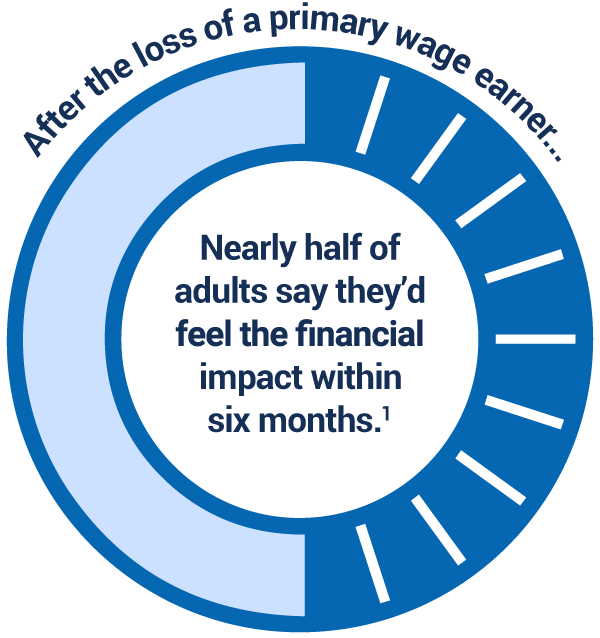

For many families, losing a primary wage earner can quickly lead to financial strain. Life insurance can be a critical safety net for those left behind by helping cover:

There are two main types of life insurance that can help protect your family. Choosing which one depends on your needs, budget and how long you need coverage.

Term life insurance provides coverage for a set number of years and is usually the most affordable option. If you pass away during that period, your beneficiaries will receive the death benefit. You may have the option to renew your term coverage or convert it to a permanent life policy.

Permanent life insurance provides coverage for your entire life and can build cash value over time. You can access this policy’s cash value while

you’re alive to help with medical expenses, emergencies or other needs.

Life insurance is for anyone who has people who depend on them

financially. This can include couples, parents, caregivers of aging parents or business owners.

Ask yourself:

1 2024 Insurance Barometer Study, Life Happens and LIMRA.

Policies are issued and underwritten by The Union Labor Life Insurance Company, Silver Spring, MD. Ullico Select, LLC is a subsidiary of Ullico Inc., the holding company, CA Lic# 0G93797.

Coverage is typically more affordable when you’re young and healthy, which means the best time to buy is right now. As life changes, your life insurance needs can change too. Major milestones can all be good times to consider or update your coverage.

The amount of life insurance coverage you need depends on your personal situation, financial goals and budget. When estimating coverage, consider final expenses, outstanding debts, everyday living costs and future needs like college or retirement.

Even if you have life insurance through your employer, it may not be enough to fully protect your family.

The cost of life insurance can depend on your age, gender, health, medical history, coverage amount and policy type. Term life insurance is usually more affordable than permanent coverage.

The best way to estimate your cost is by using a life insurance calculator to get a personalized quote.

Once you’ve figured out your coverage needs, gotten a quote and submitted your application, it will usually go through a review process called underwriting.

Traditional underwriting - Includes a medical exam and a detailed health history review. It often offers the lowest rates for healthy individuals.

Simplified underwriting - Quick application process that usually includes short health questionnaire, but no medical exam.